The Swing Overview - Week 22

Equity indices continued to rise for a second week despite rising inflation and sanctions against Russia. Economic data indicate optimistic consumer expectations and the easing of the Covid-19 measures in China also brought some relief to the markets. The Bank of Canada raised its policy rate to 1.5%. The Eurozone inflation hit a new record of 8.1%, giving further fuel to the ECB to raise interest rates, which is supporting the euro to strengthen.

Macroeconomic data

The US consumer confidence in economic growth for May came in at 106.4. The market was expecting 103.9. This optimism points to an expected increase in consumer spendings, which is a positive development. The optimism was also confirmed by data from the manufacturing sector. The ISM PMI index in manufacturing rose by 56.1 in May, an improvement on the April reading of 55.4. The manufacturing sector is therefore expecting further expansion.

On the other hand, data from the labour market were disappointing. The ADP Non Farm Employment indicator (private sector job growth) was well below expectations as the economy created only 128k new jobs in May (the market was expecting 300k new jobs). The unemployment claims data held at the standard 200k level. However, the crucial indicator from the labour market will be Friday's NFP data.

Quarterly wage growth for 1Q 2022 was 12.6% (previous quarter was 3.9%). This figure is a leading indicator on inflation. Faster inflation growth could lead to a higher-than-expected 0.50% rate hike at the Fed's June meeting.

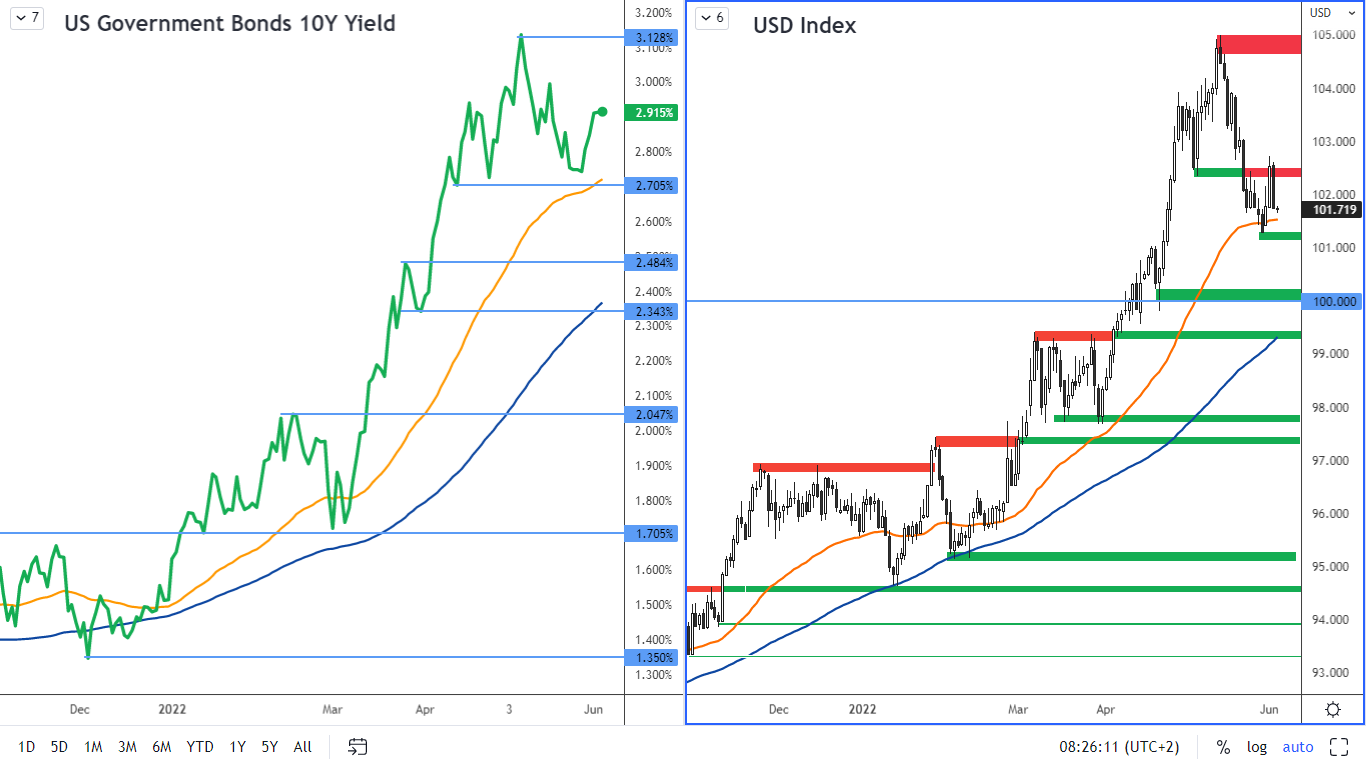

The US 10-year Treasury yields have rebounded from 2.6% and have started to rise again. They are currently around 2.9%. However, the US Dollar Index has not yet reacted to the rise in yields. The reason is that the euro, which has appreciated significantly in recent days, has the largest weight in the USD index.

The SP 500 Index

The SP 500 index has continued to strengthen in recent days. The market seems to be accepting the expected 0.50% rate hike and while economic data points to some slowdown, forward looking consumers‘ and managers’ expectations are optimistic.

Figure 2: The SP 500 on H4 and D1 chart

The US SP 500 index is approaching a significant resistance level, which is in the 4,197-4,204 range. The next one is at 4,293 - 4,306. The nearest support is at 4 075 - 4 086.

German DAX index

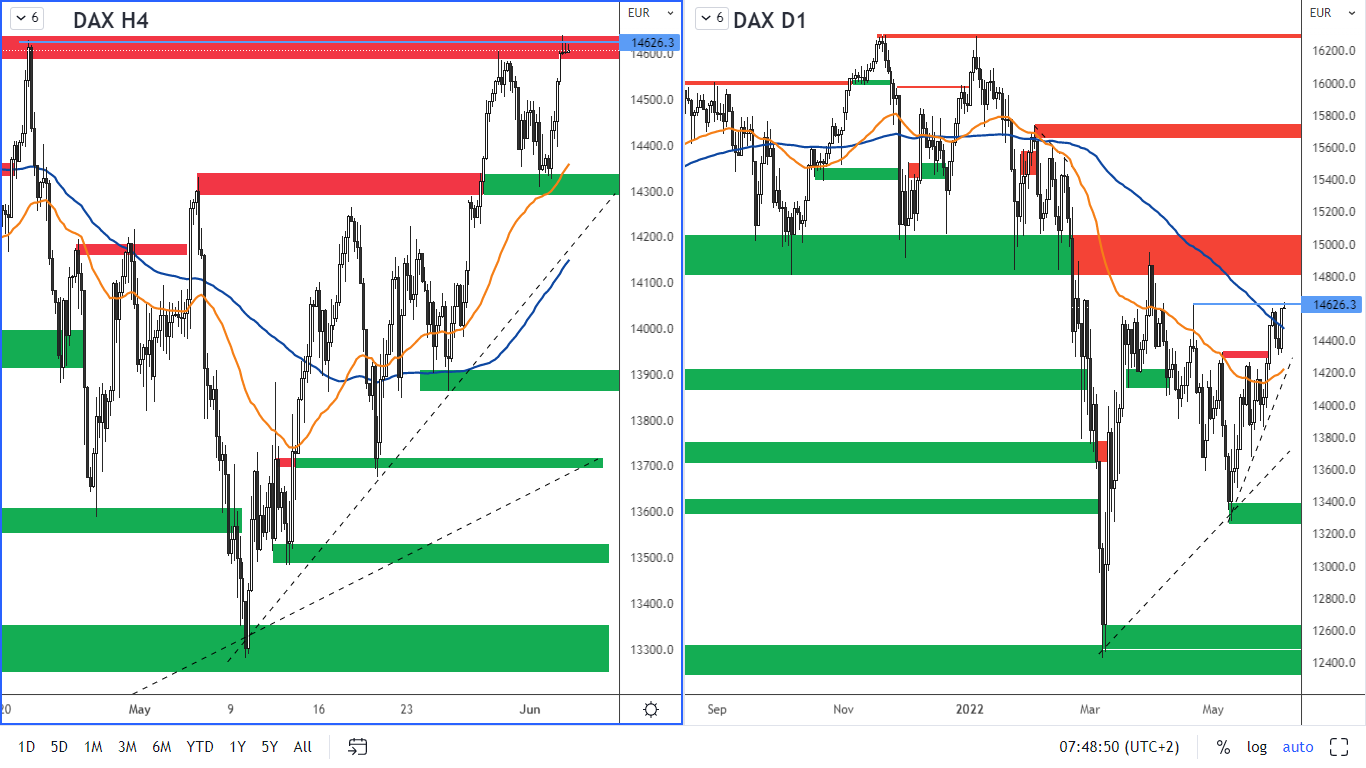

Figure 3: German DAX index on H4 and daily chart

Germany's manufacturing PMI for May came in at 54.8. The previous month it was 54, 6. Thus, managers expect expansion in the manufacturing sector. Surprisingly, German exports rose in April despite the disruption of trade relations with Russia. Exports in Germany grew by 4.4% even though exports to Russia fell by 10%. The positive data has an impact on the DAX index. However, the bulls in DAX may be discouraged by the expected ECB interest rate hike.

The DAX has reached resistance in the 14,600 - 14,640 area. The nearest significant support is at 14,300 - 14,330, where the horizontal resistance is coincident with the moving average EMA 50 on the H4 chart.

The euro continues to rise

Bulls on the euro were supported by inflation data, which reached a record high of 8.1% in the eurozone for the month of May. Inflation increased by 0.8% on a monthly basis compared to April. Information from the manufacturing sector exceeded expectations, with the manufacturing PMI for May coming in at 54.6, indicating optimism in the economy. The ECB will meet on Thursday 9/6/2022 and it might be surprising. While analysts do not expect a rate hike at this meeting, rising inflation may prompt the ECB to act faster.

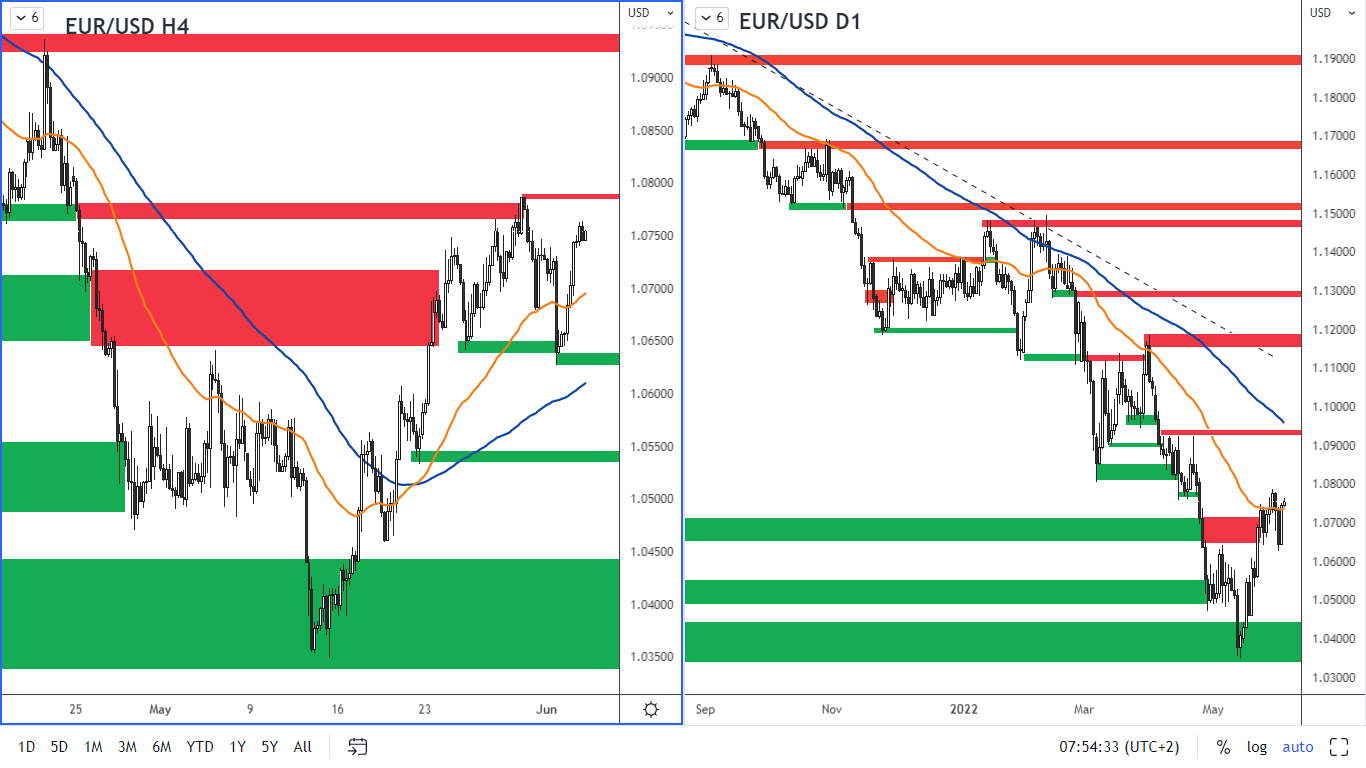

Figure 4: The EUR/USD on H4 and daily chart

The EUR/USD currency pair is reacting to the rate hike expectations by gradual strengthening. A resistance is at 1.0780 The nearest support is now at 1.0629 - 1.0640 and then at 1.0540 - 1.0550.

The Bank of Canada raised the interest rate

The GDP in Canada for Q1 2022 grew by 2.89% year-on-year (3.23% in the previous period). On a month-on-month basis, the GDP grew by 0.7% (0.9% in February). This points to slowing economic growth. Canada's manufacturing PMI for May came in at 56.8 (56.2 in April ), an upbeat development. The Bank of Canada raised its policy rate by 0.50% to 1.5% as expected by analysts. In addition to the rate hike, the Canadian dollar is positively affected by the rise in oil prices as Canada is a major exporter.

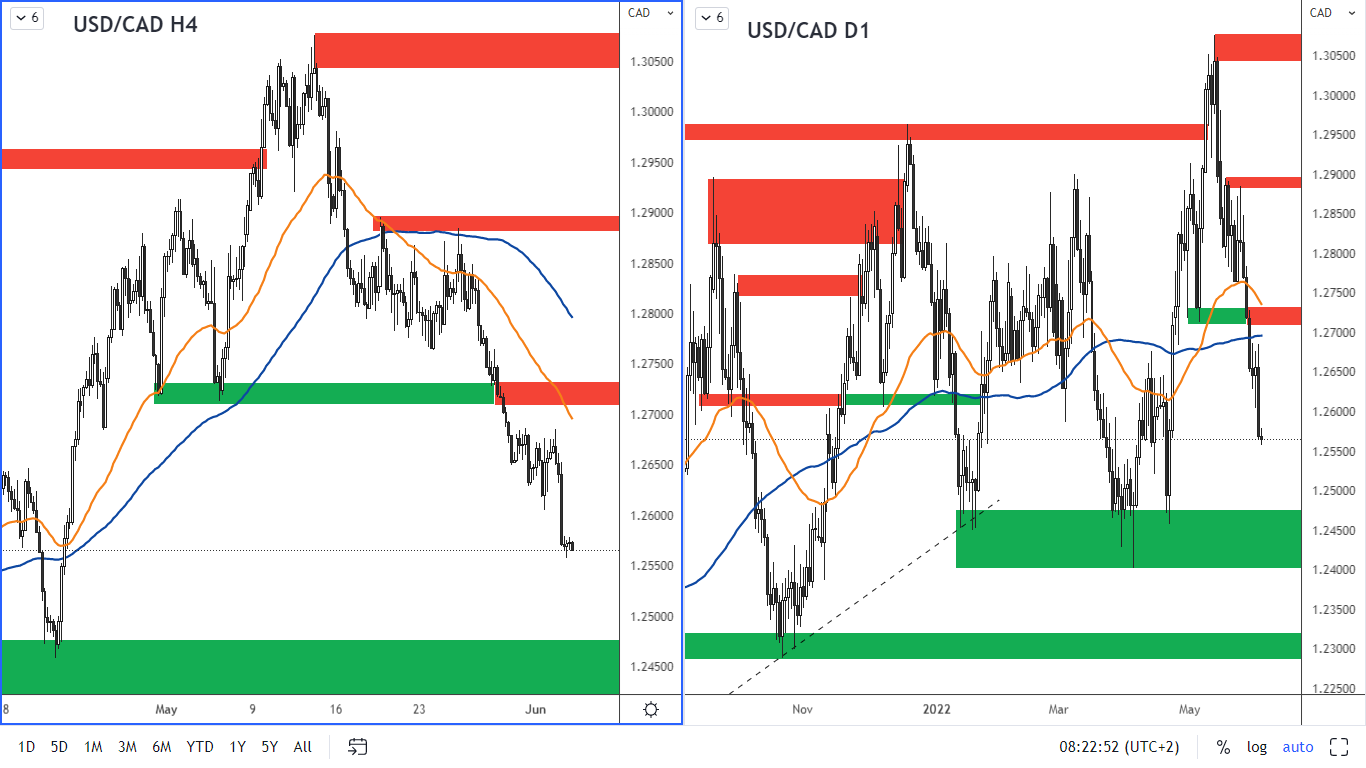

Figure 5: The USD/CAD on H4 and daily chart

The USD/CAD currency pair is currently in a downward movement. The nearest resistance according to the daily chart is 1.2710-1.2730. Support according to the daily chart is in the range of 1.2400-1.2470.

![Turbulent Q2'23 Results for [Company Name]: Strong Exports Offset Domestic Challenges](https://www.fxmag.com/media/cache/main_box_filter/uploads/articles/2022-FXMAG-COM/GPWA/gpw-s-analytical-coverage-support-programme-wse-2-6311cd4191809-2022-09-02-11-30-41-63175bda84812-2022-09-06-16-40-26.png "Warsaw Stock Exchange: Brand24 (B24) - 1Q23 financial results")

![Turbulent Q2'23 Results for [Company Name]: Strong Exports Offset Domestic Challenges](https://www.fxmag.com/media/cache/article_small_filter/uploads/articles/2022-FXMAG-COM/GPWA/gpw-s-analytical-coverage-support-programme-wse-2-6311cd4191809-2022-09-02-11-30-41-63175bda84812-2022-09-06-16-40-26.png "Warsaw Stock Exchange: Brand24 (B24) - 1Q23 financial results")