BI cuts policy rate again to support growth

Bank Indonesia has lowered its policy rate by 25 basis points to 5.00%, marking a second consecutive surprise cut. While we had expected BI to hold off on further easing until the fourth quarter – given the recent strength in GDP and CPI data, as well as weak transmission to lending rates – the move signals BI’s increasing concern over the growth outlook.

The decision also suggests that BI is taking advantage of periods of Indonesian rupiah (IDR) strength to ease policy without risking currency instability. Despite headline inflation ticking higher, it remains well below BI’s upper target of 3.5%, giving the central bank room to act pre-emptively to support domestic

Second quarter GDP surge likely to reverse in the second half of 2025

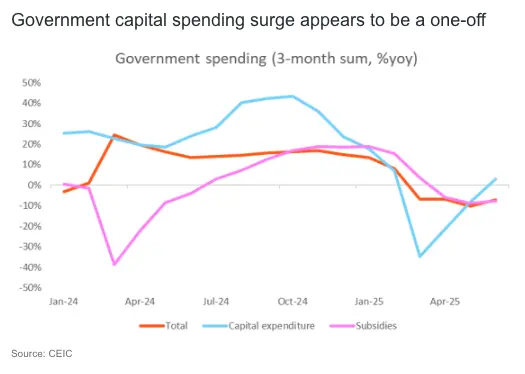

The stronger-than-expected GDP growth in Q2 was largely driven by a sharp pickup in investment, which rose 7% year-on-year compared to just 2.1% in Q1. This momentum appears to have been fueled by a significant jump in government capital expenditure, which surged 18% YoY in June 2025. However, we believe this pace is unlikely to be sustained. The revised 2025 budget projects a 3% decline in government capex for the full year.

Combined with subdued consumer spending and a projected slowdown in exports in the second half, we expect GDP growth to moderate, in line with our full-year forecast of 4.8% YoY.

Food-driven CPI spike likely temporary, but 2H CPI range to be higher

BI appeared largely unconcerned by the rise in headline CPI inflation to 2.4% YoY in July, indicating that it does not view the increase as a threat to longer-term inflation expectations. While we’re also not concerned by the July print, we expect inflation to stay above 2% in the second half of 2025 – up from 1.2% in the first half – due to reflecting seasonal trends and the fading of favourable base effects.

That said, this level of inflation remains comfortably below BI’s upper target of 3.5%, and is unlikely to derail further rate cuts

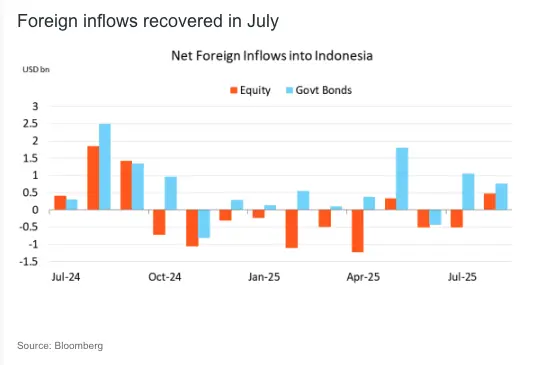

IDR stability will need continued foreign inflows as current account weakens

Although there were signs of export frontloading and a modest rebound in Q2, Indonesia’s overall trade balance deteriorated compared to Q1. This points to a likely widening of the current account deficit – not just in Q2, but also through the second half of the year – as global demand softens and terms of trade become less favourable for commodity exporters like Indonesia.

However, BI’s commitment to currency stability and foreign inflows in both government bonds and equity markets has helped IDR stabilise in a narrow range since June.

BI likely to continue easing amid weak domestic backdrop

Given the soft domestic growth outlook and our expectation that the Fed will begin cutting rates from September 2025, we believe Bank Indonesia is not yet done with its easing cycle. While the timing of the next move remains uncertain, BI may opt to front-load further rate cuts to address growth concerns, especially amid ongoing weakness in global trade and domestic consumption.

Reflecting this view, we are revising our forecast and now expect BI’s final 25bp rate cut to be brought forward from the first quarter of 2026 to the fourth quarter of 2025