Supercore progress should please the Fed

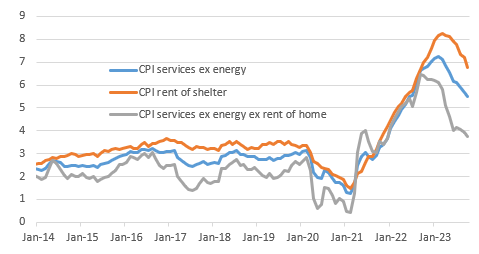

The so-called “supercore” measure of inflation – services excluding energy and housing costs – which the Fed keeps a close eye on due to wages and labour market tightness having a large influence, came in at a pretty benign 0.2% MoM rate, pulling the annual rate down to 3.75%. The Federal Reserve has got to be pretty happy with this and unsurprisingly, it has reinforced market expectations that the policy rate has peaked. Just 1.5bp of tightening is now priced by the January 2024 FOMC meeting with more than 90bp of rate cuts now anticipated by the end of next year.

Supercore inflation is making progress

Housing and vehicles to prompt further disinflation

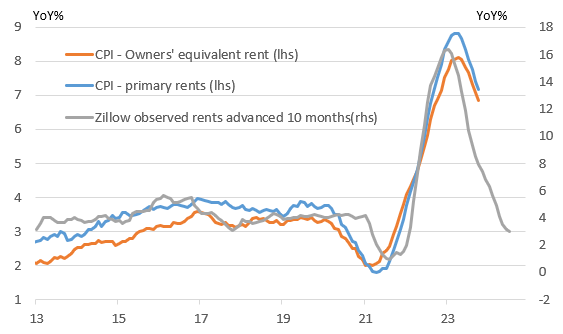

Housing rents should slow a lot further based on observed rents. If the relationship holds between observed rents and the CPI housing components, the one-third weighting housing has in the headline inflation basket and 41.8% weighting for the core rate will subtract around 1.3 percentage points of headline inflation and 1.7ppt off core annual inflation rates.

Higher credit card and car loan borrowing costs, student loan repayments and very low housing transaction numbers in an environment of weak real household disposable incomes will continue to slow consumer spending activity. Big ticket items, such as vehicles, look set to see ongoing downward pricing pressure while slower economic growth should restrict corporate pricing power more broadly in the economy. Fed Chair Jerome Powell recently acknowledged that “given the fast pace of the tightening, there may still be meaningful tightening in the pipeline”. This will only intensify the disinflationary pressures that are building in an economy that is showing some signs of cooling. We forecast headline inflation to be in a 2-2.5% range from April onwards with core CPI testing 2% in the second quarter of 2024.

Housing slowdown will increasingly depress core inflation

Scope for significant Fed policy easing in 2024

With growth concerns likely to increase over the same period, this should give the Federal Reserve the flexibility to respond with interest rate cuts. We wouldn’t necessarily describe it as stimulus but more an attempt to move monetary policy to a more neutral footing, with the Fed funds rate expected to end 2024 at 4% versus the consensus forecast and market pricing of 4.5%.

![Turbulent Q2'23 Results for [Company Name]: Strong Exports Offset Domestic Challenges](https://www.fxmag.com/media/cache/main_box_filter/uploads/articles/2022-FXMAG-COM/GPWA/gpw-s-analytical-coverage-support-programme-wse-2-6311cd4191809-2022-09-02-11-30-41-63175bda84812-2022-09-06-16-40-26.png "Warsaw Stock Exchange: Brand24 (B24) - 1Q23 financial results")

![Turbulent Q2'23 Results for [Company Name]: Strong Exports Offset Domestic Challenges](https://www.fxmag.com/media/cache/article_small_filter/uploads/articles/2022-FXMAG-COM/GPWA/gpw-s-analytical-coverage-support-programme-wse-2-6311cd4191809-2022-09-02-11-30-41-63175bda84812-2022-09-06-16-40-26.png "Warsaw Stock Exchange: Brand24 (B24) - 1Q23 financial results")