Production measures also looking promising

GDP, or more precisely GVA (gross value added) measured in terms of industrial sector production, is also with a quick look.

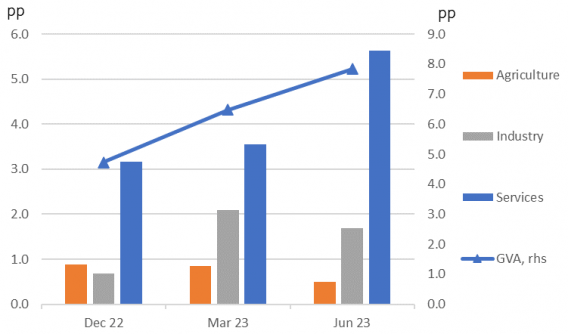

Here, we see that the main engine for growth is not industry, which has slowed a little, but the service sector. And that ties in with the consumer spending observation we made earlier. Agriculture contributed a little less this quarter - perhaps reflecting the erratic monsoons we have seen this year.

GVA by sector (contribution to growth pp)

RBI easing not a priority

Putting all of this together, it looks like the Reserve Bank of India (RBI) will be in no hurry to cut rates. Growth is clearly very strong and it looks like it will remain so in the quarters ahead. A growth rate of about 7% for the full calendar year looks probable, and something in the 6-7% range for next year is also looking likely.

The recent upward spike in inflation is, for now, almost entirely food price-driven, and there are already signs that the worst increases in tomatoes and onions are behind us, so there is equally little need for the RBI to tighten rates in response to this growth backdrop. The 6.5% policy rate will already look quite restrictive once the inflation numbers settle down again, which we believe they will do soon. Rate cuts are most likely the next direction for the RBI, but these can wait until next year.

![Turbulent Q2'23 Results for [Company Name]: Strong Exports Offset Domestic Challenges](https://www.fxmag.com/media/cache/main_box_filter/uploads/articles/2022-FXMAG-COM/GPWA/gpw-s-analytical-coverage-support-programme-wse-2-6311cd4191809-2022-09-02-11-30-41-63175bda84812-2022-09-06-16-40-26.png "Warsaw Stock Exchange: Brand24 (B24) - 1Q23 financial results")

![Turbulent Q2'23 Results for [Company Name]: Strong Exports Offset Domestic Challenges](https://www.fxmag.com/media/cache/article_small_filter/uploads/articles/2022-FXMAG-COM/GPWA/gpw-s-analytical-coverage-support-programme-wse-2-6311cd4191809-2022-09-02-11-30-41-63175bda84812-2022-09-06-16-40-26.png "Warsaw Stock Exchange: Brand24 (B24) - 1Q23 financial results")