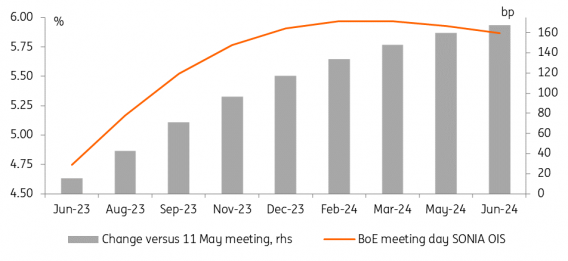

Markets have certainly reacted. In money markets, SONIA OIS pricing has shifted higher by up to 15bp since yesterday alone. A forward of 34bp higher for the upcoming meeting period implies that markets are now seeing a more than 30% chance of a 50bp hike today. The BoE reaching a terminal rate of 6% by early next year is now the market’s base case - 150bp above the current interest rate level. For comparison - and to highlight the significance of the recent shift in pricing - after the May meeting the market was looking for a peak rate of 4.75% to 5% after this summer.

The main question around this meeting for markets will be to what extent the monetary policy committee will push back against this extreme market pricing. Our economists think pushback will be unlikely. For one, the BoE appears to be just as wise about the near-term outlook of inflation as the market and is probably unwilling to pick a side for the risk of having to walk back later. And BoE officials have passed on plenty of opportunities to already do so in the recent past.

Inflation and wage data have led to aggressive market pricing of the BoE

oday's events and market view

Central banks will remain in focus, certainly with the BoE meeting today as well as the Swiss National Bank and Norges Bank decisions in the broader global picture. But we also have Fed Chair Powell’s second day on Capitol Hill giving testimony to the Senate Banking panel today. Add to that a busy slate of other speakers, where from the Fed we will hear from Christopher Waller, Michelle Bowman, Loretta Mester and Thomas Barkin, while over in the eurozone, the European Central Bank's Fabio Panetta and Luis de Guindos are speaking.

Given what is priced, the question is, of course, how much more can be priced in. As the UK CPI release has shown, data remains key. And given central banks' narrow focus, inflation data is particularly important.

Other data feeding into investors’ concerns over the longer-term outlook, with central banks potentially taking the tightening too far, could further feed into the curve flattening bias. Today’s US initial jobless claims are expected to remain elevated after they had come in higher than expected last month. Other releases today are data on US existing home sales and the Chicago and Kansas Fed activity indices. In the eurozone we get the preliminary consumer confidence reading for June.

Sovereign primary market activity today is limited to the US selling a 5Y inflation-linked bond.

![Turbulent Q2'23 Results for [Company Name]: Strong Exports Offset Domestic Challenges](https://www.fxmag.com/media/cache/main_box_filter/uploads/articles/2022-FXMAG-COM/GPWA/gpw-s-analytical-coverage-support-programme-wse-2-6311cd4191809-2022-09-02-11-30-41-63175bda84812-2022-09-06-16-40-26.png "Warsaw Stock Exchange: Brand24 (B24) - 1Q23 financial results")

![Turbulent Q2'23 Results for [Company Name]: Strong Exports Offset Domestic Challenges](https://www.fxmag.com/media/cache/article_small_filter/uploads/articles/2022-FXMAG-COM/GPWA/gpw-s-analytical-coverage-support-programme-wse-2-6311cd4191809-2022-09-02-11-30-41-63175bda84812-2022-09-06-16-40-26.png "Warsaw Stock Exchange: Brand24 (B24) - 1Q23 financial results")