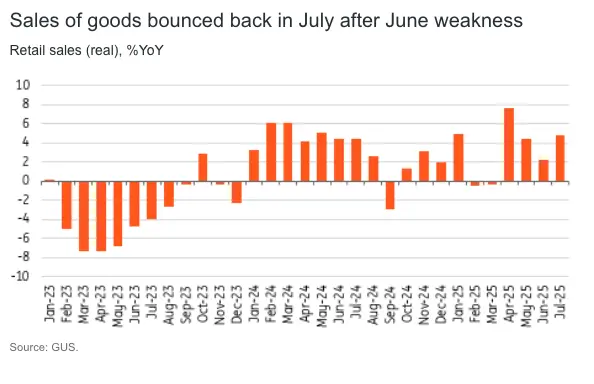

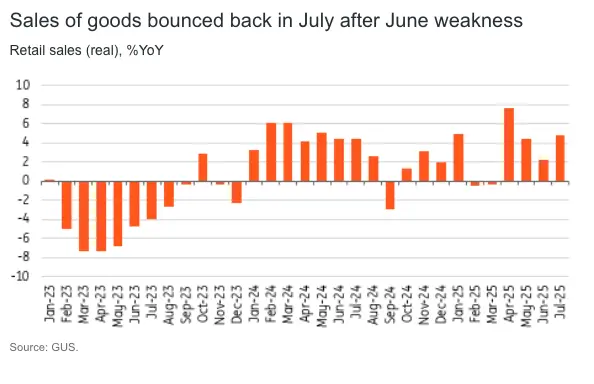

Polish retail sales of goods increased by 4.8% year-on-year in June (ING: 4.0%; consensus: 3.1%) following a small uptick of 2.2%YoY in June. Seasonally adjusted data points to stable sales in June (0.0%MoM).

Robust growth was reported in the sales of furniture, electronics and household appliances (15.3YoY), textiles, clothing and footwear (14.7%YoY) and motor vehicles, motorcycles and parts (10.7%YoY). Sales of food and beverages declined for the second month in a row in annual terms (-0.4%YoY). The implied deflator of retail sales indicates stable prices of goods after two consecutive months of annual declines.

The disappointing June sales reading prompted speculation that it could mark the reversal of a growth trend – especially in the sale of durable goods – that emerged at the beginning of the second quarter. We attributed the softer June reading to a temporary shift in consumer outlays from goods to services (including hotels and restaurants) as the Corpus Christi long weekend likely boosted demand for tourism.

The July sales report is consistent with our hypothesis and suggests that at the beginning of 3Q25, households' propensity to spend was solid and private consumption should remain the key driver of GDP growth. In 2025, we still forecast economic growth in Poland at 3.5% i.e. well above the expansion expected in other CEE economies.