First Corporate Sustainability reporting disclosures

This year marked the first Corporate Sustainability Reporting Directive (CSRD) disclosures for the 2024 financial year. The first group of entities, with more than 500 employees, had to disclose their sustainable data according to the European Sustainability Reporting Standards (ESRS). All undertakings in scope therefore disclosed information on their ESG-related impacts, risks and opportunities (IROs).

While the current scope only requires the largest entities to disclose their information, the Directive should gradually expand to all large companies, listed SMEs and EU branches and subsidiaries of non-EU companies. However, the current discussion surrounding the Omnibus I proposal questions the mere future of the regulation.

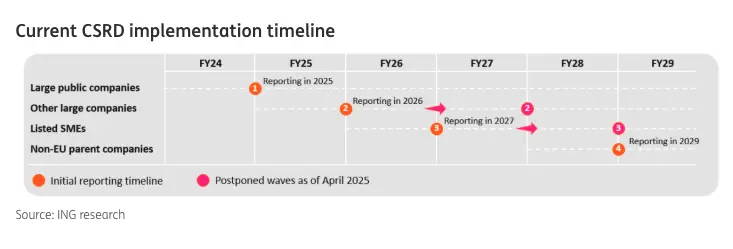

The Omnibus proposal for the CSRD includes a staggering 80% reduction in the Directive’s final scope to only include the largest corporate and financial entities. Although the legislative process is only beginning, the changes would reshuffle the number of entities required to disclose their ESG data under the CSRD. Therefore, the European legislator has already postponed the enforcement of the second and third waves of entities in scope by two years. The graph below summarises the implementation timeline of the CSRD, including the recent postponements.

Although the CSRD's future is uncertain due to the Omnibus package, we believe examining the inaugural CSRD disclosures is worthwhile.

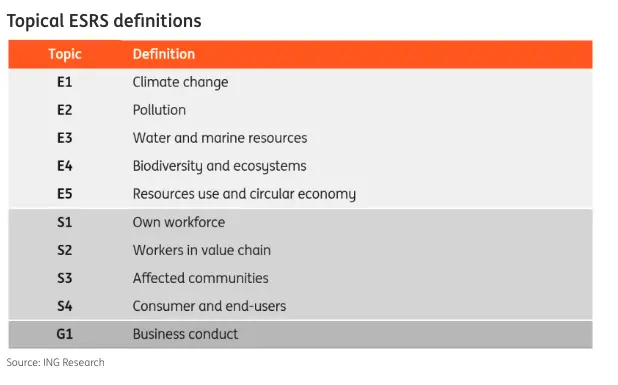

As a reminder, entities in scope were required to report on the materiality of 10 topics. The table below summarises and defines each topical ESRS. The next section dives into the results derived from our analysis of the first CSRD disclosures

It’s a messy start

For this first year of disclosures, we sampled 21 European banks and 20 corporates. Every entity dedicates a specific part of its annual report to its ESG disclosures. While those reports are easily accessible, the same cannot be said of the content itself. While this year’s CSRD disclosures were comprehensive, we noted significant differences in the way each institution disclosed its ESG information.

Major variations in the disclosure formats

More than 80% of banks and 90% of corporations in our benchmark presented their double materiality through a table format. Most companies opted to summarise the information in a table format and dedicated several sections to qualitatively describe the results. Despite this broad adoption of succinct materiality and IRO (impact, risk and opportunity) disclosure, the style, information and methodology differed significantly across our sample.

The content included in the table varied greatly with some banks and corporates including specifications on the materiality within the value chain, whether the IROs were expected or current and, in some cases, also the type of projection used (orderly transition, disorderly transition etc). These variations in reporting style greatly impeded the comparability of results.

A small share of entities included a scoring system to determine the level of materiality of each ESRS topic. Considering the major variation in the scaling, methodology and materiality thresholds of their scoring system, those were not comparable. Some corporates also described their plans and actions in some specific topics but without providing any clear assessment. Others provided statistics in relation to their activities and their needs (water, electricity, gas, specific materials) but only the knowledge of a specialist can judge the impact.

Overall, we observed significant variations in reporting style and formatting, making it extremely challenging to compare and understand the first CSRD disclosures. While the main reason for such differences is the absence of a common, harmonised reporting template, we also noted the wide variety of sustainable standards used by auditing firms.

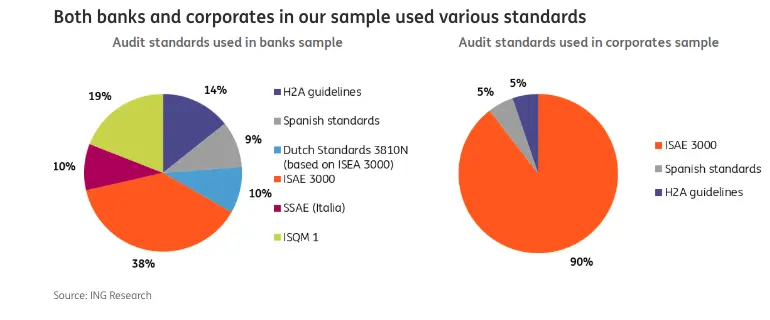

The CSRD requires all companies to have their report audited. All firms in our sample applied a limited assurance opinion, as required. The majority of those were based on ISAE 3000 standards. This is especially true for corporates, as 90% of our sample used this standard. For banks, the ratio reached only 38% of the sample. A minority of the corporates we analysed have Spanish standards and H2A guidelines.

For banks, there were national variations with six different audit standards. For example, Spanish banks were audited following the National Spanish sustainability audit standards, while Dutch banks also used a national standard based on the ISAE 3000. The graph below summarises the standards and the share each represented in our sample.

As previously noted, the formatting, methodology, and diverse audit standards of the disclosures impeded the comparability of our sample. Nevertheless, we identified several key highlights from this first year of disclosures.

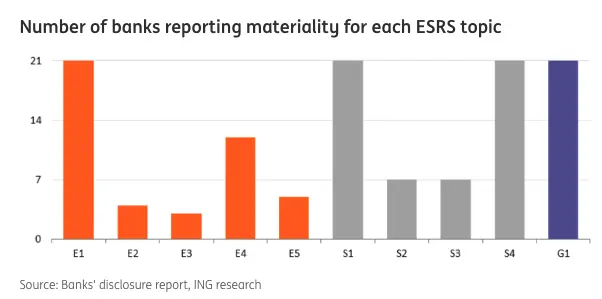

As mentioned above, banks were required to report on the materiality of 10 topics. On average, they reported 5.8 out of 10 topics as material. However, none of the banks in our sample classified all the topics as material. The only common point to all institutions in our sample is that they found materiality in ESRS E1, ESRS S1, ESRS S4 and ESRS G1 topics. The least materiality was reported for ESRS E3 and ESRS E2, with only three and four banks, respectively, finding the topics material.

We also note some national variations and trends in the total number of topics classified as material, as well as the types. Italian banks are the ones disclosing the most material topics, followed by their Dutch counterparts.

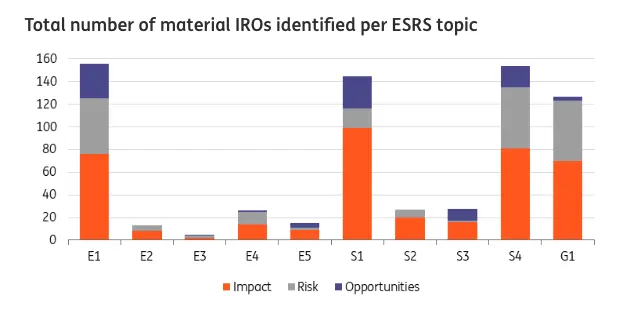

Aside from the number of topics classified as material in our sample of banks, we also noted variations in the number of impacts, risks and opportunities (IROs) reported in each disclosure. In total, we noted an average of 57 IROs reported in our sample. The graph below shows the nominal split between topics. It points out that the bulk of the materiality stems from banks’ social impact, more specifically regarding their own workers (ESRS S1) and their consumers and end-users (ESRS S4). We also note a high number of IROs identified for climate change (ESRS E1) and business conduct (ESRS G1).