Strong retail sales data showed boost from trade-in policy

China’s retail sales grew by 6.4% year on year in May, up from 5.1% YoY in April, the fastest growth rate since 2023.

The subcategories showed that consumption benefited significantly from the trade-in policy in May. The fastest growth was seen in household appliances (53.0%) and communication appliances (33.0%), both trade-in policy beneficiaries. Other beneficiary categories, such as auto (1.1%) and construction and decoration materials (5.8%), underperformed headline growth, but also recovered compared to prior months.

The "eat, drink, and play" theme recovered on the month as well, with catering (5.9%), tobacco and alcohol (11.2%), and sports and recreation (28.3%) all accelerating. This is a positive sign that the recovery is including non-policy beneficiary categories as well.

Retail sales growth, which comfortably beat market forecasts, was the bright spot of the May data dump. May's data brings the year-to-date retail sales growth to 5% YoY. It’s an encouraging sign of recovery, as policy support efforts filter through the economy. However, a more sustainable consumption recovery will likely require a turnaround of consumer confidence, which remains much closer to historical lows than historical averages. A negative wealth effect and continued cost-cutting remain key headwinds.

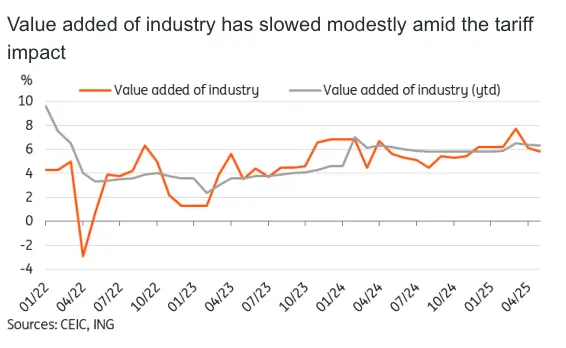

Value added of industry moderated in May

The value added of industry moderated to 5.8% YoY in May, down from 6.1% YoY in April, reaching a 6-month low. This slowdown was well expected, however, as the previous few months benefited from trade frontloading and tariff impacts continue to feed through to export and manufacturing.

Manufacturing growth remained resilient at 6.2% YoY. Hi-tech sectors in particular outperformed with 8.6% YoY growth in May. By industry, rail, ships and planes (14.6%), autos (11.6%), electrical machinery (11.0%), and computers and communication equipment (10.2%) outperformed. In contrast, we saw a sharp slowdown in textiles (0.6%). This suggests China's low-end manufacturing may be taking a bigger hit from elevated tariffs. Meanwhile, high-end production remains insulated as the end market is either not focused on the US or sees sticky enough demand.

Despite the slowdown, year-to-date growth remains quite solid at 6.3% YoY, and industrial activity has somewhat surprisingly remained a growth driver through the first half of the year.

Fixed-asset investment slumped amid heightened uncertainty

Fixed-asset investment (FAI) slumped to 3.7% YoY year-to-date in May, down from 4.0% YoY ytd in April.

Public-led FAI continues to outperform with a 5.9% YoY ytd growth, while private investment growth stalled, coming in flat at 0.0% YoY ytd. Foreign investment continued to shrink, down -13.4% YoY ytd.

By sector, manufacturing FAI remains the main bright spot, up 8.5% YoY ytd, led by investments in auto (23.4%) and rail, ship, and airplane (26.1%) manufacturing.

Investment is seeing a clear impact from global uncertainty. Considering that fixed-asset investment is often made with a multi-year horizon in mind, uncertainty about tariffs and the economic outlook may be leading to heightened caution. This includes greenlighting new investments, while the general environment of cost-cutting is also likely contributing to the slowdown.